How much is $10000 worth in 10 years at 5 annual interest?

future value of $10000 - imagine you tuck $10,000 into an account today and forget it for ten years. What will be in that account when you come back? The short answer depends on the interest rate, how often interest is added, and the inflation that affects buying power. This article walks you through the math, shows annual and monthly compounding examples, adjusts for inflation, and gives practical tips you can use right away.

Why the future value of $10000 matters

The future value of $10000 is more than a number on a statement: it tells you how much your savings can grow and what that growth means in real purchasing power. Knowing this helps you set realistic goals, choose accounts or investments, and plan for taxes and fees.

Tip: For clear, beginner-friendly calculators and tutorials, check FinancePolice’s main site for guides that match this walkthrough: FinancePolice. It’s a straightforward place to test the numbers and read practical explanations.

The basic formula: compound interest in plain language

Compound interest means interest earns interest. The standard formula is simple:

FV = PV × (1 + r)^n

Where: PV is the present value (your $10,000), r is the annual rate in decimal form (5% = 0.05), and n is the number of years (10). That formula gives the nominal future balance.

Step-by-step: annual compounding at 5%

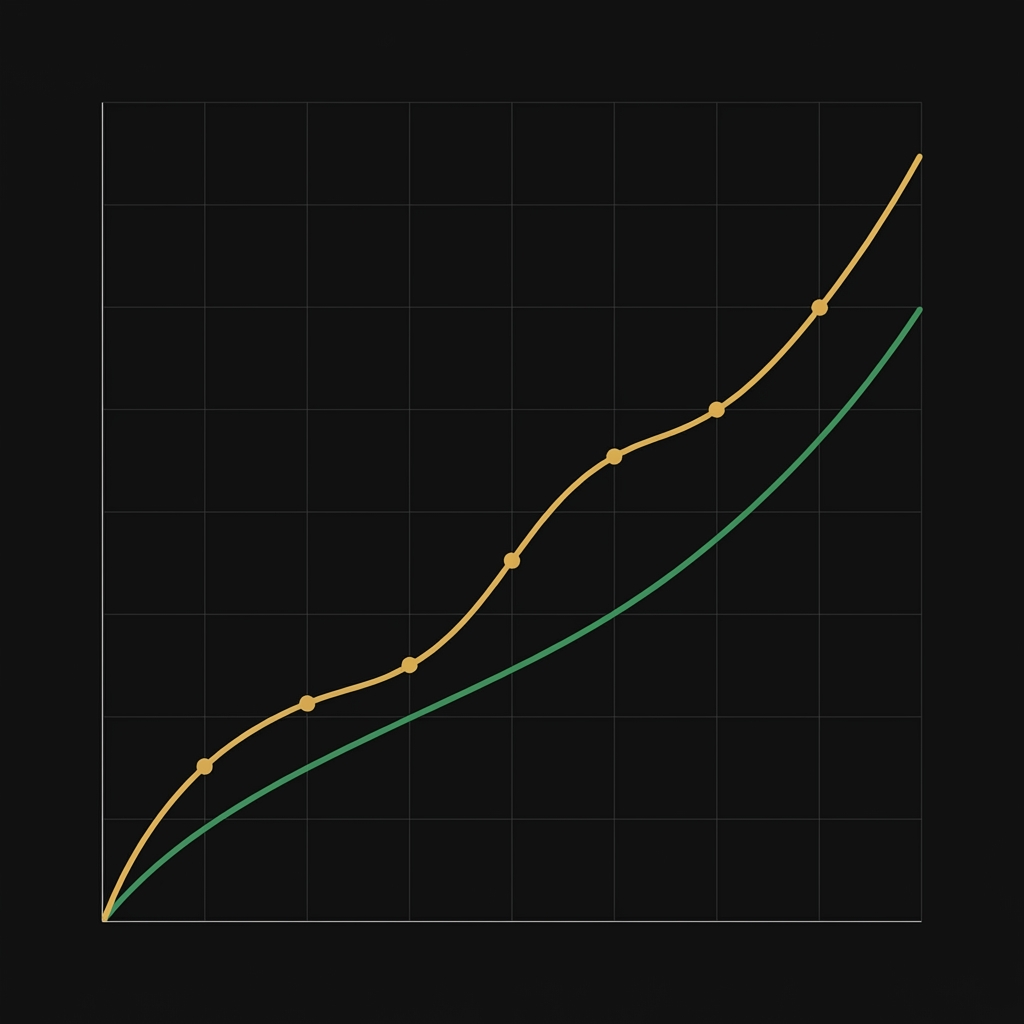

Plug in the numbers: (1 + 0.05)^10 = (1.05)^10 ≈ 1.6288946268. Multiply by $10,000 and you get about $16,288.95. That figure is the nominal result if interest is credited once per year.

Yes - that result is the straightforward future value. If you want to reproduce it in a spreadsheet, use PV*(1+r)^n and you’ll get the same number.

Monthly compounding: a small but real boost

When interest compounds more often, it slightly increases your effective return. For m payments per year the formula becomes:

FV = PV × (1 + r/m)^(m×n)

For monthly compounding (m = 12) at 5% over 10 years, compute (1 + 0.05/12)^(120) ≈ 1.647009006. That gives about $16,470.09. The difference from annual compounding is roughly $181 over ten years - real, but modest.

Effective annual rate explained

The effective annual rate (EAR) converts a quoted nominal rate with periodic compounding into a true annual rate you can compare. For 5% nominal compounded monthly:

EAR = (1 + 0.05/12)^12 − 1 ≈ 5.116%

So the monthly compounding effectively yields about 5.116% per year, explaining the slightly higher FV.

Think in purchasing power: adjusting for inflation

A nominal future value tells you how many dollars you’ll have. To know what those dollars can buy, adjust for inflation. Use:

Real FV = Nominal FV / (1 + inflation)^n

With a 3% inflation assumption over 10 years, (1.03)^10 ≈ 1.343916379. Divide the annual-compounded $16,288.95 by that factor and you get roughly $12,120 in today’s dollars. Using the monthly-compounded $16,470.09 gives about $12,257. That shows the 5% nominal rate translates to about a 1.94% real return when inflation runs 3%.

Yes, but only a little. Monthly compounding at the same nominal rate yields a slightly higher effective annual rate (about 5.116% for 5% nominal), which produces a modestly larger future balance over time. The practical takeaway: compare effective annual rates (EAR), not just nominal rates, and factor fees and taxes into your decision.

Real vs. nominal rates: the Fisher relation

If you prefer inflation-adjusted thinking, use the Fisher equation:

Real rate ≈ (1 + nominal) / (1 + inflation) − 1

With 5% nominal and 3% inflation: (1.05 / 1.03) − 1 ≈ 1.94% real. Growing $10,000 at ~1.94% for ten years gives the same inflation-adjusted result as converting nominal to real afterward.

Why that perspective helps

Thinking in real rates simplifies planning if your goal is to preserve or grow buying power. Use the real rate when comparing investments across different inflation assumptions or when your objective is specific purchasing goals rather than raw dollar totals.

Practical scenarios: quick comparisons you can use

Below are compact examples you can reproduce quickly.

Example A — 5% annual

PV $10,000 → FV ≈ $16,288.95 nominal → real ≈ $12,120 (with 3% inflation).

Example B — 5% monthly

PV $10,000 → FV ≈ $16,470.09 nominal → real ≈ $12,257 (with 3% inflation).

Example C — 3% annual

PV $10,000 → FV ≈ $13,439 nominal → real ≈ $10,000 (with 3% inflation).

Example D — 7% annual

PV $10,000 → FV ≈ $19,671 nominal → real ≈ $14,626 (with 3% inflation).

These scenarios show how just a couple percentage points in nominal return change outcomes significantly over a decade.

Taxes, fees and other practical adjustments

Don’t forget taxes: interest in taxable accounts is often taxed as ordinary income. If your 5% nominal is in a taxable account, your after-tax rate might be much lower depending on your bracket. Retirement accounts have different rules, so the after-tax effect varies.

Fees and minimum balances also matter. A higher nominal rate can be negated by regular fees or poor account terms. When you compare offers, compute the effective after-fee, after-tax rate where possible.

A simple checklist before you commit

Use this checklist when thinking about how to grow $10,000 over ten years:

1. Confirm whether the rate is nominal or already an effective rate (EAR).

2. Check compounding frequency (annual, monthly, daily).

3. Estimate inflation for your planning horizon and compute the real return. Try low/base/high scenarios (e.g., 2%, 3%, 4%).

4. Account for taxes and fees to get an after-tax real return.

5. Re-run the math in a spreadsheet and save scenarios for review.

How to reproduce the math in a spreadsheet

Open a new sheet and enter:

Cell A1: 10000 (PV)

Cell A2: 0.05 (r)

Cell A3: 10 (n)

Cell A4 (annual): =A1*(1+A2)^A3

Cell A5 (monthly): =A1*(1+A2/12)^(12*A3)

Cell A6 (real): =A4/(1+0.03)^A3

That reproduces the examples shown earlier and lets you change r, n, or inflation to test alternative paths.

Continuous compounding and limits

Continuous compounding is the mathematical limit as compounding frequency grows without bound. The formula uses Euler’s number e:

FV = PV × e^(r×n)

For 5% over ten years: e^(0.05×10) = e^0.5 ≈ 1.648721, giving FV ≈ $16,487.21. That’s only a little higher than monthly compounding, which shows the gains from increasing compounding frequency have a finite limit.

Choosing accounts and investments for real goals

Which vehicle best grows the future value of $10000? It depends on your goal and risk tolerance and the types of investments you consider:

Savings accounts and CDs: Low risk, predictable nominal rates (often quoted as APY). Good for short-term, emergency funds, or when capital preservation is key.

Bonds: Moderate risk and return; interest and principal depend on issuer credit and interest-rate movement.

Stock market: Higher expected returns over long periods but with volatility; not guaranteed.

Hybrid or target-date funds: Useful if you want a hands-off option aligned with a time horizon.

Always choose an instrument whose realistic expected return reflects your planning assumption. If you plug 5% into the formula but buy a savings account that typically yields 1% historically, numbers won’t match reality.

Why running multiple scenarios matters

Because inflation, taxes, and returns are uncertain, the best practice is to run at least three scenarios: conservative, base, and optimistic. For example:

Conservative: 3% nominal return, 3% inflation → real ≈ 0%

Base: 5% nominal, 3% inflation → real ≈ 1.94%

Optimistic: 7% nominal, 3% inflation → real ≈ 3.88%

Seeing these side-by-side helps you choose savings rates and risk levels that match your goals. If preserving purchasing power is the goal, conservative scenarios will show how much extra saving may be required.

Common reader questions, briefly answered

Is monthly compounding worth changing banks for?

Usually not by itself. The difference between annual and monthly compounding at the same nominal rate is small. Focus first on higher nominal rates, lower fees, and better account terms. Then use compounding frequency as a tie-breaker.

Should I use a single inflation assumption?

Start with a single assumption for convenience but also run variants. Inflation forecasts can change; scenario planning reduces unpleasant surprises.

Can I treat this math as a prediction?

No. These calculations show what will happen if your assumptions hold. They are tools for planning, not guarantees.

Where to check numbers and find calculators

Trusted sources include government and educational sites with calculators and clear explanations: Investor.gov (SEC), the Bureau of Labor Statistics CPI tools, and Khan Academy. Finance-focused publishers like Investopedia and Bankrate offer interactive calculators too. Also try Calculator.net to run specific interest scenarios. A small tip: look for the site's logo to quickly return to your saved tools.

A short tax example to show the drag

Suppose the 5% nominal interest is taxed at 24% each year in a taxable account. Your after-tax rate becomes about 3.8% (0.05 × (1 − 0.24) = 0.038). Growing $10,000 at 3.8% for ten years gives FV ≈ 10,000*(1.038)^10 ≈ $14,607. After adjusting for 3% inflation, real buying power falls to about $10,871. Taxes matter.

Anecdote: the surprise of nominal comfort

A relative once tucked $10,000 into a conservative account and checked back ten years later. The balance looked comforting - until inflation-adjusted value was computed. The nominal rise hadn’t translated to much extra buying power. The lesson: compare nominal gains with realistic inflation and tax estimates.

Simple rules of thumb

1. Convert quoted rates to effective annual rates to compare products.

2. Use the real rate for planning that targets purchasing power.

3. Run multiple inflation scenarios (2%–4%) to see sensitivity.

4. Don’t let compounding frequency distract from bigger drivers: nominal rate, fees, and taxes.

Test your savings scenarios with clear, practical tools

Ready to test your own scenarios? Try FinancePolice’s guides and calculators for clear examples and step-by-step walkthroughs, or visit the advertising page to learn how FinancePolice can help share practical tools: Advertise with FinancePolice.

Final practical walkthrough you can copy

Open a spreadsheet and set these cells: PV = 10000, r = 0.05, n = 10. For annual compounding use =PV*(1+r)^n. For monthly: =PV*(1+r/12)^(12*n). For real value with inflation i: =NominalFV/(1+i)^n. Save the file so you can tweak r and i to test conservative vs optimistic paths.

Resources to learn more

Try Investor.gov for official tutorials, the Bureau of Labor Statistics CPI tools for inflation series, Khan Academy for lessons on compound interest, and well-known calculators on Investopedia and Bankrate to compare compounding options.

Closing thought

Understanding the future value of $10000 is a small but powerful step toward clearer financial decisions. Use the formulas here, try multiple scenarios, and remember to factor in taxes and fees. That will make your planning realistic and reduce surprises when you check your balance a decade from now.

At 5% annual compounding, $10,000 grows to about $16,288.95 after ten years. To find the inflation-adjusted value, divide that nominal amount by (1 + inflation)^10. For a 3% inflation rate, the purchasing power is roughly $12,120 in today’s dollars.

Monthly compounding yields a slightly higher future value because interest is added more frequently. At 5% nominal interest, monthly compounding over ten years gives about $16,470.09 versus $16,288.95 with annual compounding — a difference of roughly $181. The gain is real but modest; focus first on higher nominal rates, lower fees, and tax treatment.

Reliable places to run these numbers include Investor.gov (SEC educational resources), the Bureau of Labor Statistics CPI tools for inflation data, Khan Academy’s compound interest lessons, and calculators on Investopedia or Bankrate. FinancePolice also offers straightforward walkthroughs and practical examples you can use to test assumptions.

References

- https://financepolice.com

- https://financepolice.com/advertise/

- https://financepolice.com/category/investing/

- https://financepolice.com/how-to-budget/

- https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

- https://www.bankrate.com/banking/savings/compound-savings-calculator/

- https://www.calculator.net/interest-calculator.html